Accountant or Lawyer? What No One Tells You When Starting Your Startup

Discover why a consultancy isn't a substitute for a lawyer in the startup world. Learn what each one does and how to avoid serious legal mistakes.

Read more →

The MICA Regulation has brought a key transformation to the European crypto ecosystem: the obligation to publish a whitepaper — also known as a libro blanco — for public offerings of cryptocurrencies. This practice, which until now was common but voluntary, becomes a legal requirement under certain conditions, especially for issuers operating in Spain or within the European Union market.

In this article, we analyze when a whitepaper is mandatory, what it must include, how it is notified, which rules govern advertising, and what rights consumers have.

Traditionally, the whitepaper has been the informal document that crypto projects used to explain their value proposition. However, the MICA Regulation turns it into a mandatory instrument for cryptocurrency issuers (except in specific cases), establishing requirements regarding content, format, and advertising.

MICA refers to it as a libro blanco, but in legal and technical practice, it is the mandatory whitepaper required to launch a cryptocurrency lawfully.

All legal entities that carry out a public offering of cryptocurrencies (other than stablecoins or e-money tokens), except in the following cases:

In addition, public offerings of utility tokens may only be carried out within a maximum period of 12 months.

The MICA Regulation requires that every whitepaper must include at least:

Additionally:

In Spain, if the project is neither a stablecoin nor a token linked to electronic money, the issuer must:

This notification must also include the planned advertising communications.

Advertising of cryptocurrency offerings — now regulated by Article 6 of MICA — must adhere to principles of truthfulness and consistency with the whitepaper.

The regulation requires that:

Any subsequent modification to the whitepaper must:

MICA introduces a significant consumer protection right: the right of withdrawal. Article 12 states that the buyer has 14 calendar days to cancel their cryptocurrency purchase without reason or cost.

Issuer obligations:

When does this right not apply?

The cryptocurrency whitepaper evolves from being an informal marketing tool to becoming a central legal requirement under MICA. Its purpose is not only to formalize offerings but also to ensure transparency, reduce fraud, and protect consumers.

Although it imposes more obligations on issuers, it also fosters trust, professionalizes the sector, and provides a predictable framework for investment. Ultimately, it is another step toward a stronger, more transparent, and more attractive European crypto market.

Discover why a consultancy isn't a substitute for a lawyer in the startup world. Learn what each one does and how to avoid serious legal mistakes.

Read more →

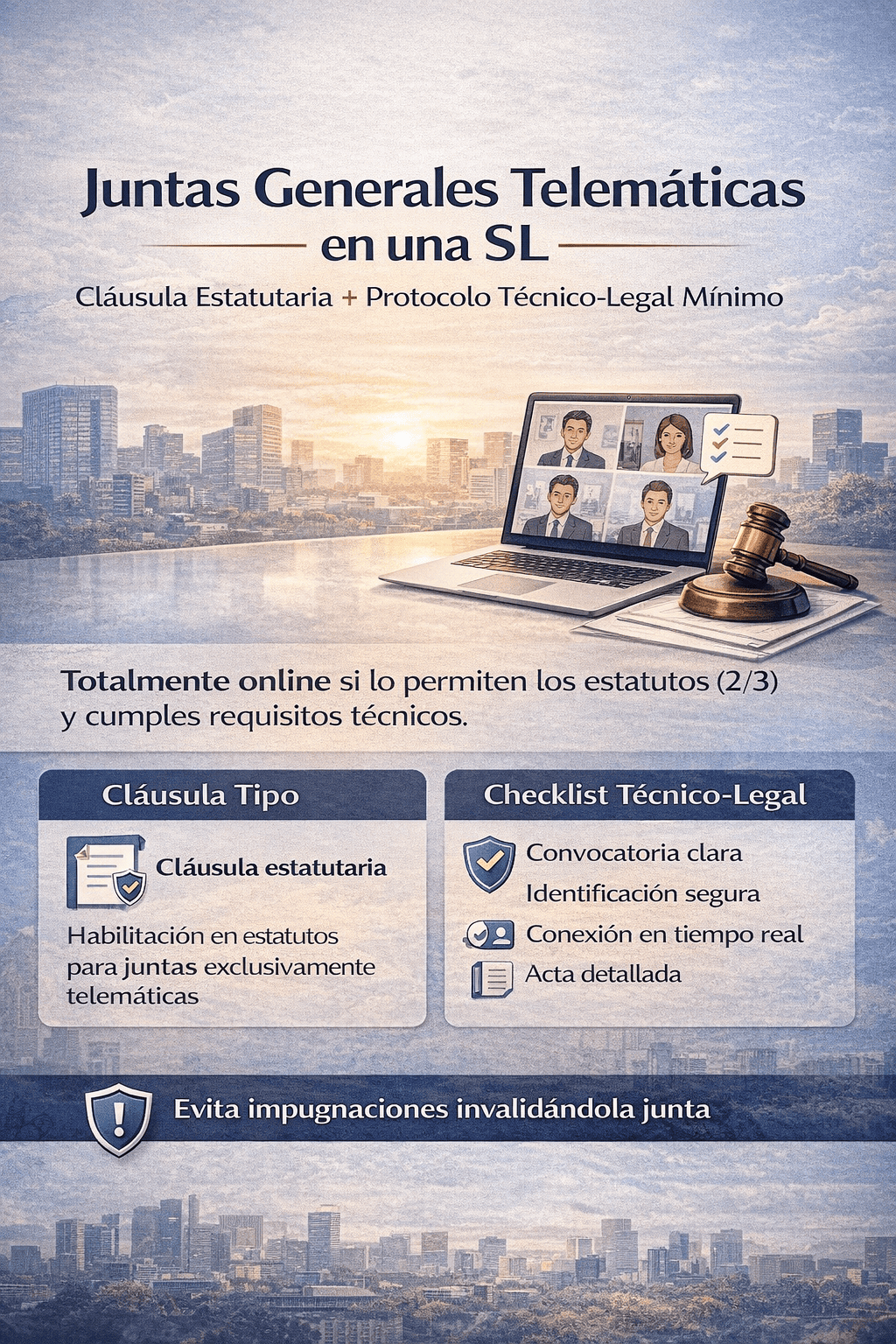

Practical guide for companies in Spain: when you can hold fully online general meetings in an SL, whether you need to amend the bylaws, a sample clause, checklist and protocol to avoid challenges.

Read more →

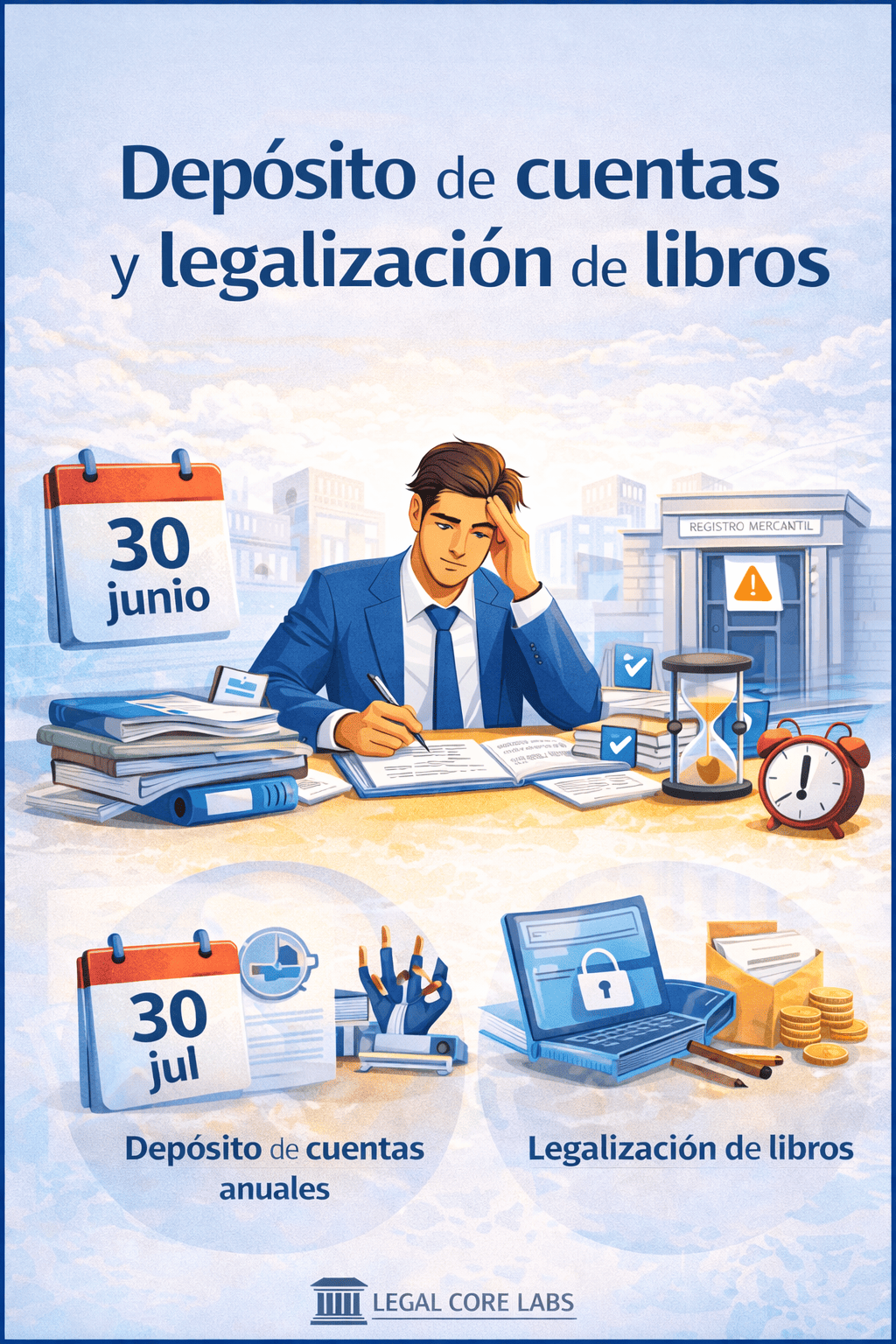

Clear, practical guide for startups and tech companies in Spain: when to file annual accounts, how to legalise corporate books, what happens if you miss deadlines (Registry block, ICAC fines) and a checklist to stay compliant.

Read more →