Anti-dilution clauses in startups: Full Ratchet vs. Weighted Average explained

Learn how anti-dilution clauses work in startup investment deals, the risks of Full Ratchet vs. Weighted Average, and how to negotiate them under Spanish law.

Read more →

For startups, corporate housekeeping often sits behind product, revenue, fundraising and hiring. The issue is that Spanish corporate compliance has two recurring obligations that do not stay in the “we will do it later” bucket. If you neglect them, you can end up with a Commercial Registry block, economic penalties, and serious friction in funding rounds, audits, banking and procurement.

The two key obligations are:

These obligations apply broadly in Spain (startups and traditional SMEs alike). What changes is the practical impact: a Registry block can stop the transactions startups need most (capital increases, director changes, powers of attorney, option plans, due diligence).

This guide explains what to do, when to do it, what happens if you miss deadlines, and how to prevent issues.

Main legal references (Spanish):

LSC (Companies Act, consolidated): https://www.boe.es/buscar/act.php?id=BOE-A-2010-10544

Commercial Code: https://www.boe.es/buscar/act.php?id=BOE-A-1885-6627

RD 2/2021 (ICAC penalty criteria): https://www.boe.es/buscar/act.php?id=BOE-A-2021-1351

LGT (tax formal obligations and penalties): https://www.boe.es/buscar/act.php?id=BOE-A-2003-23186

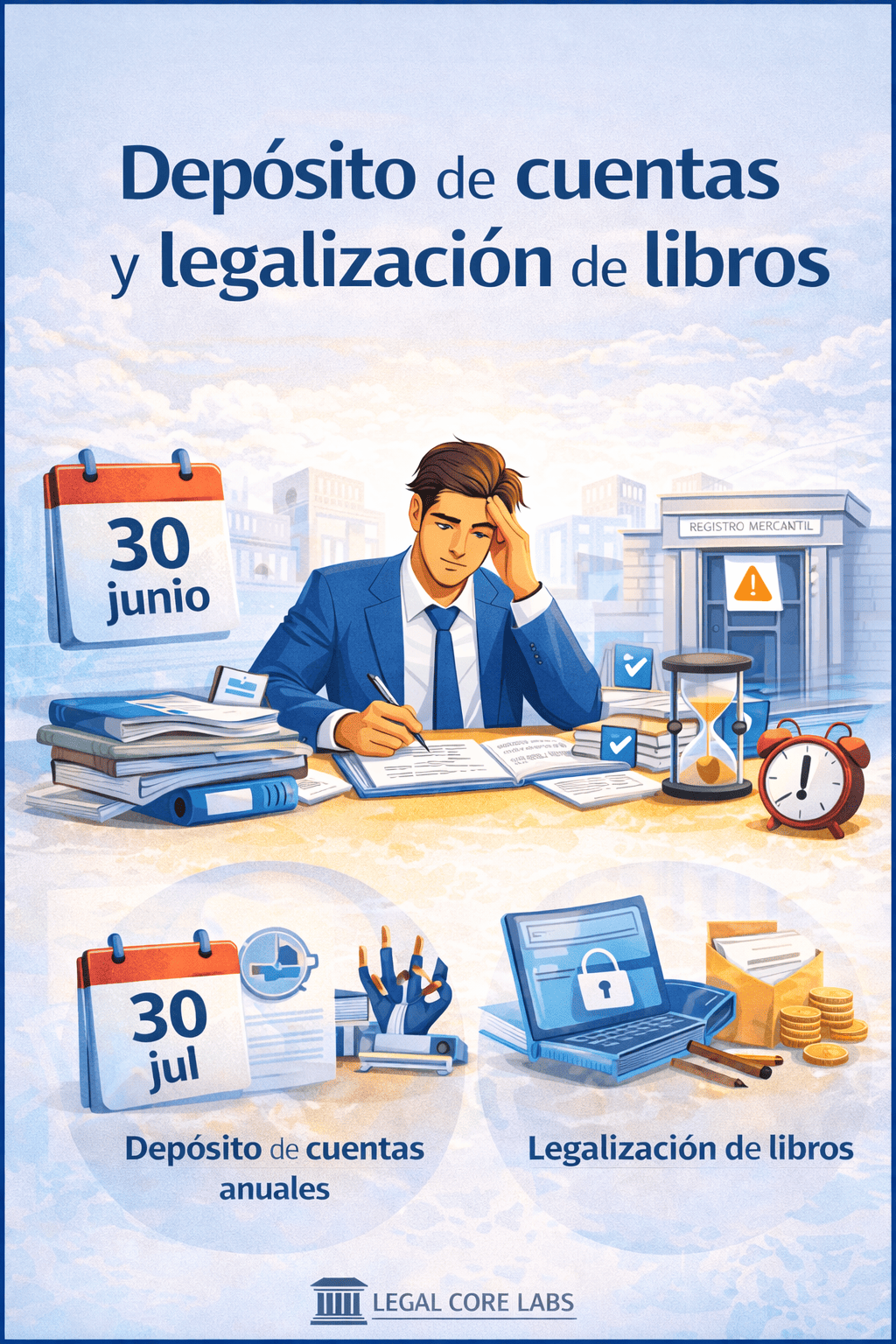

In Spain, companies must file their annual accounts with the Commercial Registry. This is part of the transparency model: accounts become publicly accessible and the Registry records compliance.

If your financial year ends on 31 December, a typical calendar is:

Practical rule: if approval happens on 30 June, aim to file before 31 July.

Depending on company size and audit requirements, filings typically include:

If you fail to file, Spanish law can trigger a Registry block. While non-compliance persists, the Registry will generally refuse to register company documents (LSC).

This affects typical startup actions:

Key exceptions: certain entries may still be registered (for example, director resignations/removals, revocation/renunciation of powers, dissolution and liquidation related entries, and entries ordered by a court or public authority).

In addition to the block, there is a sanction regime. The statutory range is 1,200 to 60,000 euros (LSC). If the company (or group) exceeds 6,000,000 euros in annual turnover, the maximum can rise to 300,000 euros per year of delay (LSC).

Royal Decree 2/2021 provides practical criteria often applied in proceedings:

For most startups, the bigger risk is not only the fine, but the Registry block and the reputational impact in fundraising and due diligence.

Spain requires companies to keep mandatory books and to legalise them through the Commercial Registry (today, largely electronic and submitted telematically).

The Commercial Code sets a key timing requirement: mandatory books must be legalised within 4 months after the end of the financial year. If year-end is 31 December, the practical deadline is 30 April.

For a Spanish private limited company (SL), this usually includes:

Accounting books

Corporate books

In single-member structures, an additional “contracts with the sole shareholder” register can be relevant where applicable.

It helps to distinguish corporate consequences from tax risk.

If you legalise books late, the Registry typically records that the submission is out of time. This is not always an automatic monetary fine, but it can create friction in:

Spain’s General Tax Law (LGT) includes formal obligations and penalties tied to accounting and registers. In audits or disputes over accounting reliability, missing or poorly maintained books can worsen your position and may expose the company to sanctions.

Accounts are not filed. You try to register a capital increase for investors. The Registry block prevents registration until you regularise.

Books were not legalised on time. Investors ask for additional warranties, indemnities, or holdbacks, because corporate hygiene is not “deal ready”.

Shareholder conflict blocks approval. Filing is delayed and the Registry block risk increases exactly when the company needs flexibility.

If everyone owns it, no one owns it. Assign it to finance (CFO), operations, or an external advisor with internal follow-up.

Signatures, certificates, financial statements, management report and audit report where applicable.

Opportunity cost (fundraising, banking, powers, corporate actions) usually exceeds administrative costs.

Late legalisation and weak corporate records can become expensive in disputes or transactions.

Within one month after shareholder approval (LSC).

Within the first six months after year-end (LSC). Late meetings may still be valid, but non-compliance creates risk.

A Commercial Registry block can prevent registrations and the ICAC may impose fines (LSC).

No. Certain entries can still be registered (for example, director resignations/removals, revocation of powers, dissolution and liquidation, and court-ordered entries).

Within 4 months after year-end (Commercial Code).

Not necessarily as a direct corporate fine, but the Registry record and the associated tax and evidentiary risks can be material.

Need to put your corporate calendar under control, regularise overdue filings, or get your company “due diligence ready” for investors?

At Legal Core Labs we help startups and tech companies in Spain with annual compliance planning, Registry filings and risk prevention so corporate housekeeping does not slow down the business.

Learn how anti-dilution clauses work in startup investment deals, the risks of Full Ratchet vs. Weighted Average, and how to negotiate them under Spanish law.

Read more →

Practical guide in Spain for moving from sole trader to Sociedad Limitada: how to transfer assets and contracts, tax implications, legal steps and operational considerations for a smooth transition.

Read more →

Practical guide to voting thresholds in Spanish private limited companies (SL): what passes with ordinary majority, what needs over 50% or 2/3, key minority rights (1%, 5%, 25%) and how to align bylaws and shareholder agreements without creating gridlock.

Read more →